Options Scanner

Overview

dxFeedRadar Options Scanner is a powerful SaaS platform that enables real-time scanning of the entire equities and options universe using a wide variety of criteria. The Options Scanner solves some of the financial industry’s most challenging questions:

How to find the right investment instruments

How to get real-time trading triggers

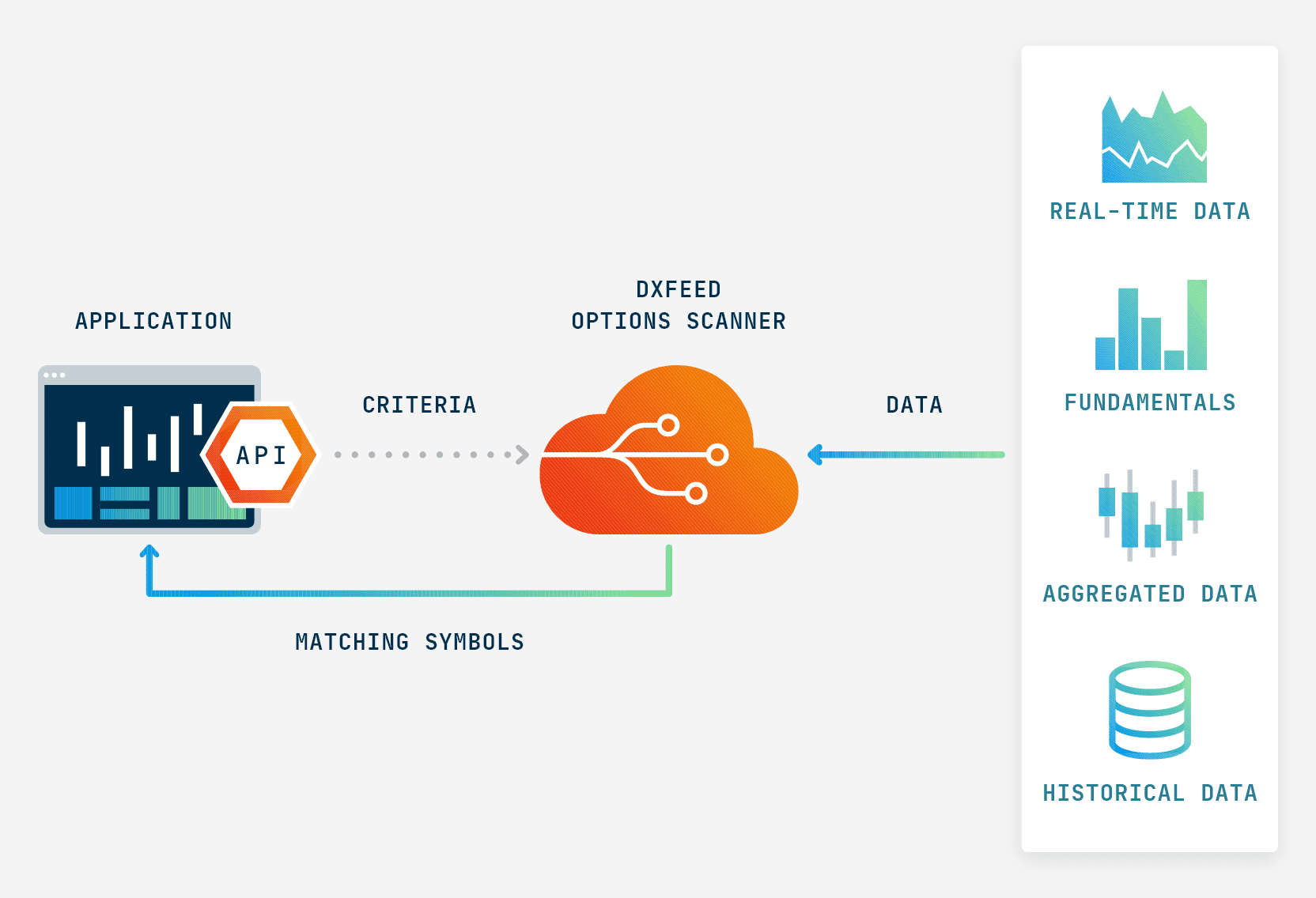

dxFeed Options Scanner can be connected to your application or website using REST API. Searches are performed in tick resolution using real-time data from all major US and European exchanges. An extensive range of options parameters (e.g., Greeks, IV, and theoretical option prices) and underlying fundamentals can be used for searching. Clients are provided with the powerful dxScript language to build their own search criteria.

Benefits

A powerful SaaS platform that enables instrument searches via seamless REST API integration

Unbeatable coverage, supporting 2mln+ instruments: the entire universe of US and European equities and options

An extensive set of pre-built data points, including theoretical options pricing, Greeks and IV calculation, VIX and ATM IV

Unique dxScript programming language for time series analysis to set more targeted criteria

Low latency data feeds through dxFeed residing in the closest proximity to exchanges

Consulting & expertise

24x7 Support

How it works

Features

Main features of dxFeed OptionsScanner:

150+ supported data points

100+ supported requests per minute, each scanning 2mln+ instruments, equities, and options to find a match. Horizontally scalable for more

Leverages all dxFeed OPRA feed capabilities and the dxFeed infrastructure to deliver relevant and the most accurate search result possible

The Options Scanner makes it possible to use all the data for filtering, sorting, and fetching actual values. The data can also be used to create custom market expressions (e.g., ratios or differences), and they can be used anywhere else in the request.

Data available in the OptionsScanner:

Options descriptive data

Symbol, underlying, CFI, expiration, strike price

Theoretical prices

Model-free approach to receive theoretical options prices that:

Enter into the existing bid/ask if possible

Are arb-free

Are extrapolated when no quotes exist

Greeks and implied volatility

Calculated using the Black-Scholes model

Aggregated data

Latest daily candles

Historical indicators

Average volumes, prices, historical volatilities, technical indicators

Aggregations of options data on the underlying level

Сall, Put, total volume, and open interest. VIX and ATM implied volatility, calculated for an option series closest to the required residual maturity

Maturity curves on the underlying level

Time value, strike moneyness per option, implied volatility by time to expiration

All data available for underlyings

Fundamentals, Prices & Candles, Quotes, and more

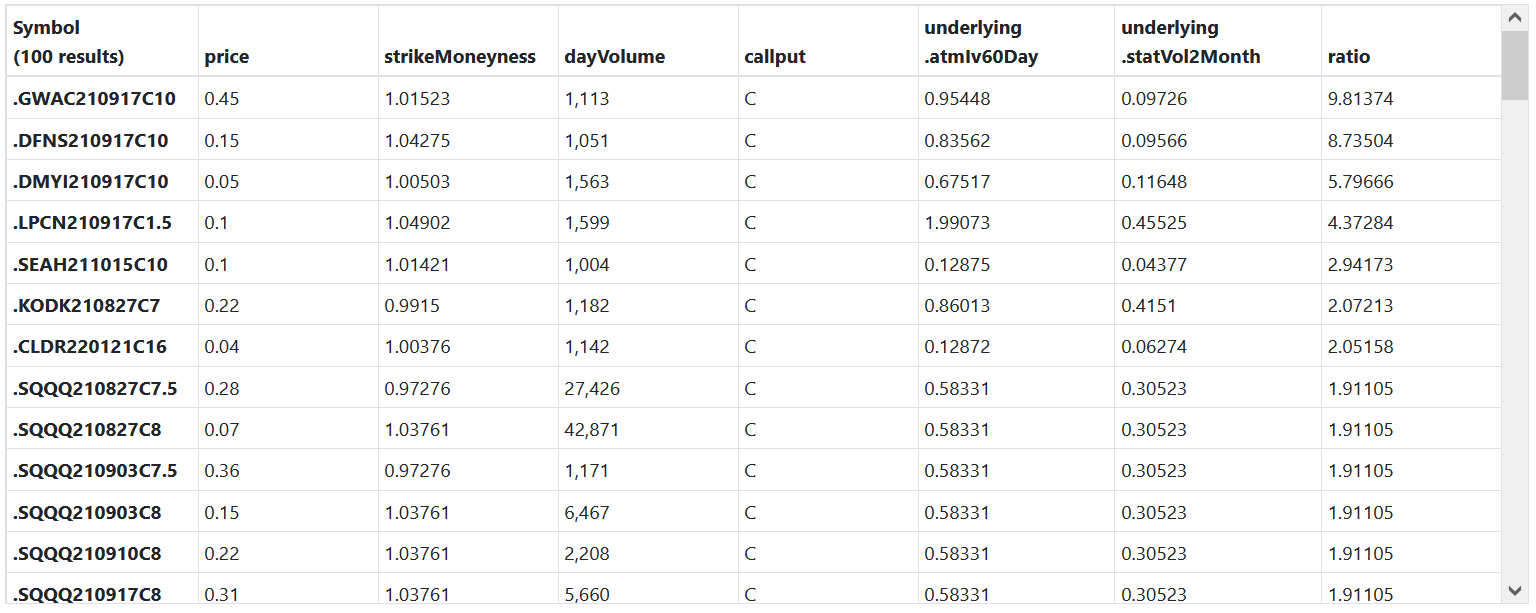

Use case: option strategy based on IV to SV ratio

Description

In modern financial markets, it is becoming increasingly difficult to keep up with the flow of information. The right set of tools is often the key to understanding what’s important and what’s not. This is especially true in the case of option markets where the number of outstanding contracts is enormous.

Here we examine one possible scenario of options analysis using dxFeed Options Scanner.

The ratio of implied (IV) and statistical (SV) volatility of the underlying security measures the relation between the theoretical and the market price of the option. A high ratio indicates the option is overpriced (e.g, investors treat the asset as a hedge) and vice versa (e.g., insufficient liquidity).

If the ratio is sufficiently high, (e.g., greater than 1.3), it is a possible sign that option-selling strategies are viable. There’s a range of applicable approaches, such as selling the naked or covered option, or shorting the straddle (a combination of a call and put), to name a few. While the choice of a particular strategy is up to each trader’s style and risk preference, dxFeed Options Scanner allows them to quickly highlight cases for further analysis. We would also like to narrow our search down to the options near the money, with a strike price between 0.95 and 1.05 of the latest available price of the underlying security.

Using dxFeed Options Scanner

Choose the options data points to receive:

price

symbol

Select the data points that will be used to find options you are interested in:

underlying.atmIv60Day = the implied volatility of an ATM option with a residual maturity of 60 days

underlying.statVol2Month = the annualized historical standard deviation of logarithmic returns, calculated based on 2 calendar months

strikeMoneyness = the ratio between the options strike and the latest available price of its underlying security

dayVolume = current day volume of the instrument

callput, Call or Put

To get the ratio between ATM IV and SV, create a new mathematical expression:

ratio: underlying.atmIv60Day / underlying.statVol2Month

Add filters to the desired attributes. In this case, we are interested in near the money call options with sufficient trading volume and a high IV to SV ratio:

a ratio greater than 1.3

strikeMoneyness between 0.95 and 1.05

dayVolume greater than 1000

callput equals (call)

The results will be returned with the data for selected data points. For example, the result might be presented as follows:

Request

The actual API request will look like:

{

"instrumentCategory": "OPTION",

"datapoints": [

{

"expr": "callput"

},

{

"expr": "price"

},

{

"expr": "dayVolume"

},

{

"expr": "strikeMoneyness"

},

{

"expr": "underlying.atmIv60Day"

},

{

"expr": "underlying.statVol2Month"

},

{

"expr": "underlying.atmIv60Day / underlying.statVol2Month",

"name": "ratio"

}

],

"filters": [

{

"datapoint": 0,

"alternatives": [

{

"predicate": "==",

"args": [

"C"

]

}

]

},

{

"datapoint": 2,

"alternatives": [

{

"predicate": ">",

"args": [

"1000"

]

}

]

},

{

"datapoint": 3,

"alternatives": [

{

"predicate": "[]",

"args": [

"0.95",

"1.05"

]

}

]

},

{

"datapoint": 6,

"alternatives": [

{

"predicate": ">",

"args": [

"1.3"

]

}

]

}

],

"sorters": [

{

"datapoint": 6

}

],

"outputs": [

{

"datapoint": 0

},

{

"datapoint": 1

},

{

"datapoint": 2

},

{

"datapoint": 3

},

{

"datapoint": 4

},

{

"datapoint": 5

},

{

"datapoint": 6

}

]

}